The Price of Immortality

Or why some companies seemingly never die

Companies are pretty cool. They are, as Coase might have put it, individuals brought together through a governance charter to do things they couldn't easily do alone or with too high transaction costs. But they're often fickle, and fail to adapt to the changing world.

Geoffrey West, of the Santa Fe institute in his studies of scaling laws says in the section where he applies it to companies:

An extrapolation of the theory and data predicts that the probability of a company’s lasting for one hundred years is only about forty-five in a million, and for it to last two hundred years it’s a minuscule one in a billion. These numbers should not be taken too seriously, but they do give us a sense of the scale of long-term survivability and provide an interesting insight into the characteristics of companies that have remained viable for hundreds of years. There are at least 100 million companies in the world, so if they all obey similar dynamics, then one would expect only about 4,500 to survive for a hundred years, but none for two hundred.

He also went on to say that this is clearly not true. There are firms that have been around for much longer. But re those, West thinks:

Most of them are of relatively modest size, operating in highly specialized niche markets, such as ancient inns, wineries, breweries, confectioners, restaurants, and the like.

So I took a look at these types of companies who seem to defy death to see if this conception holds up.

1. The forever companies

Japan is interesting in so many ways. But one of the most interesting is the fact that the country has 33,000 businesses that are at least a century old! Often called shinise meaning "old shop", many have been around for much much longer. For instance, Tsuen Tea in Kyoto has been a going concern since 1160 AD. They survived for almost a millennium by doing one thing and one thing only (serving tea, in case that was unclear). Their current owner says:

We’ve focused on tea and haven’t expanded the business too much. That’s why we’re surviving.

And they're not alone. Japan also has:

The oldest hotel in the world, open since 705 in Yamanashi

Confectioner Ichimonjiya Wasuke selling sweet treats in Kyoto since 1000

Hosoo, a kimono manufacturer started in 1688

And a way longer list of companies that are older than most countries.

One common trend amongst most of these companies is that they are dedicated to doing one thing and one thing well. There's little ambition to grow, to expand, or to try new things. Sure they might change recipes, or remix ingredients, or have minor variations on what can be served in the tea house, but in essence, what's being provided in the year 2020 is very similar to what would've been provided a century ago, or a millennium ago.

From Wikipedia:

According to a report published by the Bank of Korea in 2008 that looked at 41 countries, there were 5,586 companies older than 200 years. Of these, 3,146 (56%) are in Japan, 837 (15%) in Germany, 222 (4%) in the Netherlands, and 196 (3%) in France. Of the companies with more than 100 years of history, most of them (89%) employ fewer than 300 people.

And there are more. For instance, have a glance at the oldest firms in major countries.

(Yes after looking at this I like Canada even more than I did before)

2. The innovative giants

And it's not just the little mom and pop shops either. Once we bring the average age down to a century of two, we see a few larger companies.

A construction giant Takenaka, founded in 1610

Suntory and Nintendo, both born in the 1800s

A BBC article states:

Many of these oldest companies are medium or small family-owned organisations focusing on hospitality and food, like Tsuen Tea. Several companies have even benefited from the widely-accepted Japanese practice of adopting adult male workers into the family bloodline to ensure an unbroken succession for the business, something even huge firms like Suzuki Motor and Panasonic have done.

Then there are companies like GE, started in 1892, who still exist as large ongoing concerns. After having been started by Thomas Edison to do work in electricity related fields, they expanded over the years to Aviation, Capital, Digital, Nuclear energy, Healthcare, Power and Finance.

A funny coincidence (?) is that there are plenty of banks and insurance companies in this group. There are 231 banks that started before 1900s. The oldest is, of course, in Italy where Banca Monte dei Paschi di Siena in Florence founded in 1624. Bank of England started in 1694. Bank of Scotland started in 1695. But more recently, Schroders started in 1804, Rothschild & Sons started in 1811. State Bank of India started in 1806.

Similarly for insurance, its beginning was with property insurance. The Great Fire of London started the trend in 1666, and as a result Nicholas Barbon started fire insurance in 1681. Things started roughly around the same time abroad as well:

Hamburger Feuerkasse is the first officially established fire insurance company in the world, and the oldest existing insurance enterprise available to the public, having started in 1676

Later, the life insurance industry in the US started in the 1760s, where Presbyterian Synods in Philadelphia and New York founded the Corporation for Relief of Poor and Distressed Widows and Children of Presbyterian Ministers in 1759. Then the other priests started comparable relief funds alongside. The same motif continued with Accident insurance, National insurance, and more!

Non-commercial entities

Things get even more interesting when you look at the non-commercial entities. For instance, started in 930AD, and as the longest running parliament in the world, Iceland has almost everyone beat. Maybe San Marino should also deserve a mention. Despite it being small enough to jump across, they do have written documents dating back to before Constantine, to 301 AD.

Even the British Empire can date back to Magna Carta in 1215, but that, as far as I can tell, required a fair bit of colonialization to ensure continuation.

Summary

The conclusion of this little digression has been to find common grounds amongst the most long lived organisations, and turns out you need to be a particular type of company:

Extreme dedication to doing one thing well

Whether it's running a tea shop in Kyoto or a bank in Florence, the same principles seem to apply. You focus all your energies on doing one thing well, get known for it, and remain small intentionally so that all you keep doing is that one thing.

Could Tsuen Tea expand? I'm sure it could! Which Private Equity wouldn't want to fund that expansion? But they don't. Because that would dilute the whole brand and value proposition. Small, well known, artisanal endeavours with long histories don’t duplicate themselves well.

Focus on survival above other considerations

GE, Suzuki, Mitsubishi and others of its ilk focused on survival rather than "core competencies". They were happy to open up new areas of businesses, almost seemingly at random. The young whippersnapper Samsung, only started in 1938, has already gone through iterations of being focused on being a trading company, food processing, textiles, insurance, and now emergent in technology! Even in electronics they refocused regularly, going from televisions, to audio, to phones and beyond.

The literature on conglomerates more broadly, which these companies could be considered as, states that they are not ideal investments in many cases because of the inherent diversification of income streams they offer. That's what creates the conglomerate discount. There's a paper by Lewellen that suggests that "the conglomerate merger between two firms is warranted to the extent that the diversification effect of combining two income streams reduces the probability of bankruptcy."

But the very fact that they have inherent diversification of relatively independent revenue streams is also what makes them more resilient. They do what makes money and are fearless about exploring their adjacencies. That's why Yamaha can make pianos and motorcycles, and Samsung makes buildings and cellphones. They're not bound by much apart from the motivation to make money.

Coda

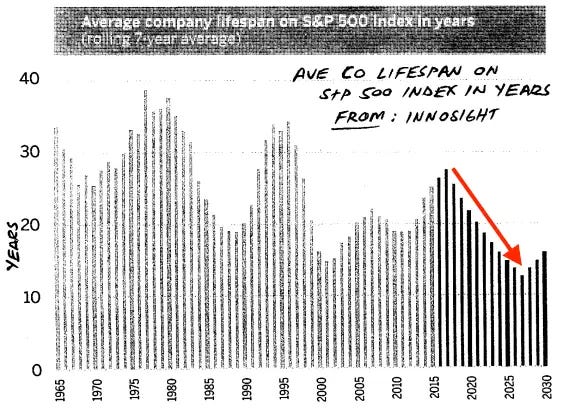

One metric I wish existed is something I’ve started calling Company Lifetime Value, just like customer lifetime value or employee lifetime value. It's the cumulative profit that a company can and will generate over its lifetime. Now normally it's artificially circumscribed by our investment horizons and lifespan, so there's a point it just becomes asymptotic, but nonetheless I've found it useful to figure out what type of an organisation it is I’m dealing with.

In that frame, having a company that has the ability to survive for longer periods of time is an advantage. It is a natural way to hedge against the fact that our publicly traded companies are seeing their lifespans come down.

And the way to do that is to find companies like GE who can survive anything. Which, funnily enough, makes them look a lot more like cities rather than companies.

Geoffrey West in his analysis of scaling laws affecting companies, organisms and cities writes:

Although there are significant differences, it’s hard not to be struck by how similar the growth and death of companies and organisms are when viewed through the lens of scaling—and how dissimilar they both are to cities. ... The fact that companies scale sublinearly, rather than superlinearly like cities, suggests that they epitomize the triumph of economies of scale over innovation and idea creation. ... In contrast, cities embody the triumph of innovation over the hegemony of economies of scale. ... They operate in a much more distributed fashion, with power spread across multiple organizational structures from mayors and councils to businesses and citizen action groups. No single group has absolute control. As such, they exude an almost laissez-faire, freewheeling ambience relative to companies,

Companies, as we understand them, have mission statements and a purpose. They have a vision led by a founder or CEO and they have at least some semblance of understanding as to what their "focus" should be and their "core competencies" are.

Part of the answer is surely that they want to provide predictability to employees and investors in terms of what they are going to do. Circumscribing the possible actions help with justifying and understanding the future.

But surely do what makes money is a better defining characteristic?

Are there other companies out there that do similar things? Probably. Berkshire Hathaway is one. There's no justification or vision beyond invest in great companies. KKR does this too, they just want to find a deal, and don't care at all whether the company is in technology or healthcare or oil.

But Microsoft isn't going to go start a restaurant chain. And Facebook won't go start a semiconductor manufacturing plant.

Imagine if you're the city of Miami. You make your recurring revenue services from attracting companies to relocate and taxing them. Do you care if the companies that come over are in social media or semiconductor or auto or a restaurant chain? All you care is that they come, get set up, employ people and you get to collect taxes.

In other words they only optimise for the revenues, and don't care at all about how that's brought in.

The price of immortality is staying small and in your lane. The price of longevity is to continually hunt for the next dollar wherever you can, and be ruthless with your sacred cows, with limited guarantee of success even then. The price of following your passion and charging ahead in a given direction, that prize is the Elvis Presley of prizes - to live fast, die young, and leave a good looking corpse.

Or you could start a bank. Those things look like they never die!

Its great to know information through this read and thanks for the share Rohit. Any insights as to what makes these companies survive for over 100 years. Any similarities found? or is it a cultural thing. If survival does mean focussing on a core competency then what else can it be?